Key Points at a Glance

Penalty for Tax Evasion: Monetary penalty or imprisonment up to 5 years, in particularly severe cases up to 10 years. Summons or Search? Remain silent and contact a specialist attorney for tax criminal law. Voluntary Disclosure: When properly executed, it can lead to exemption from punishment. Amount of Evasion Can Affect Sentencing Range: From €50,000 onwards, the accusation of a particularly severe case is imminent. Specialized Criminal Defense: Our firm specializes in tax criminal law nationwide.

Tax Evasion: A Criminal Offense with Social Relevance

Hardly any property crime has received such public attention in recent years as tax evasion. Prominent cases such as that of Uli Hoeneß or the Cum-Ex complex have brought tax criminal law into the focus of public perception. Annually, the tax investigation authorities initiate approximately 30,000 investigation proceedings.

Suspicion of Tax Evasion – Concerning Yourself or Others

You are accused of tax evasion or you have indications of irregularities – whether in your own company or in your professional environment?

Before you provide any information to the authorities or even consider voluntary disclosure or filing charges against third parties, you should urgently seek legal advice. Hasty steps – even well-intentioned ones – can significantly worsen your own legal position. We review your situation discreetly, legally secure, and with a clear focus on the best defense strategy.

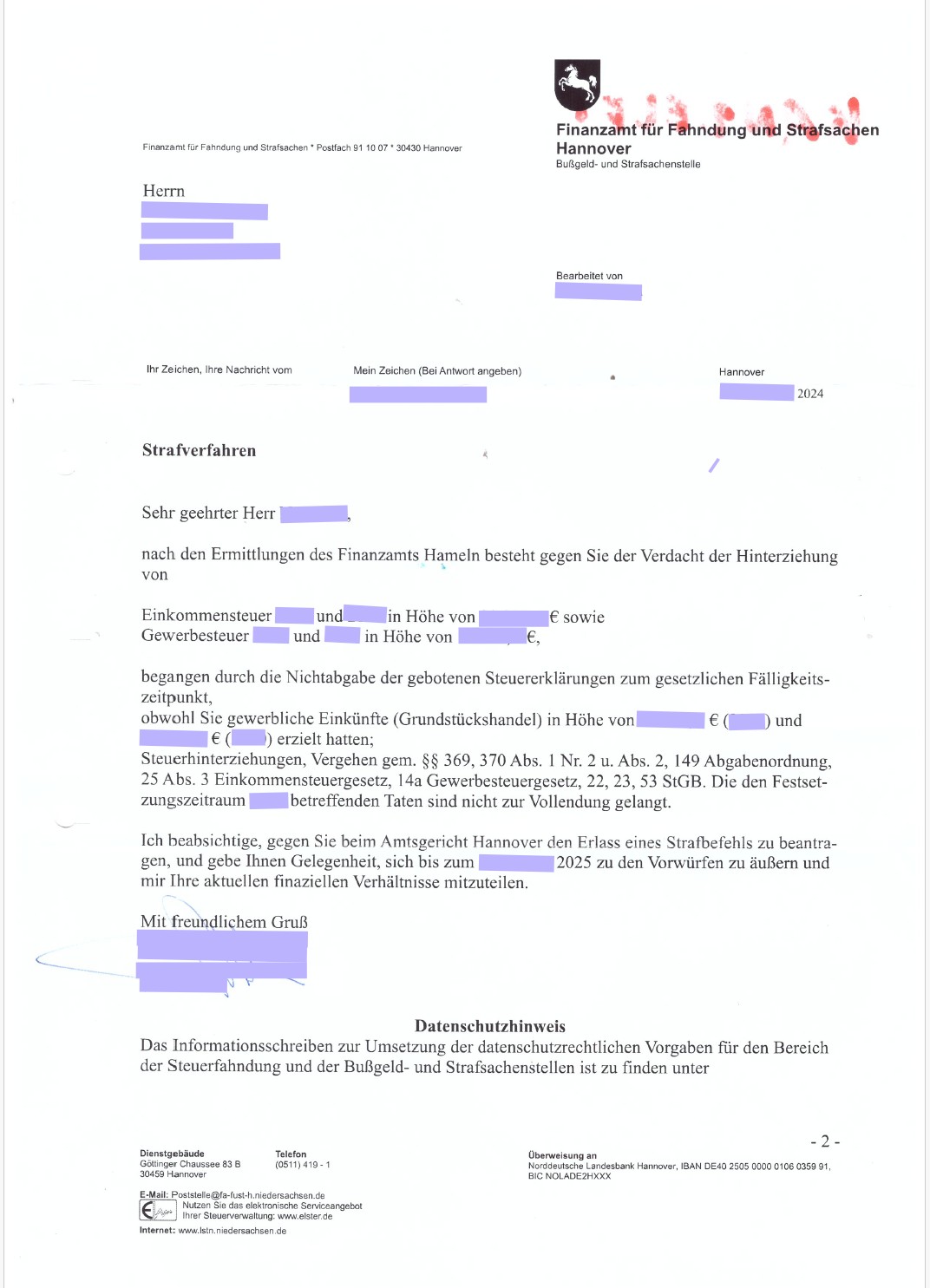

Summons or Search – Your Rights

If you receive a summons from the Tax Office for Investigation and Criminal Matters or are affected by a search:

-

- Remain silent – you are not required to provide any information.

- Do not hand over any documents or PINs before an attorney has reviewed everything.

- Stay Calm

- Contact a specialist attorney for criminal law and tax law or certified specialist advisor for tax criminal law.

- We will immediately request access to the files and develop a defense strategy.

Immediate Assistance in Case of Summons or Search

Nationwide representation – with clear focus on tax criminal law and economic criminal law.

When does tax evasion occur?

According to Section 370 (1) AO , tax evasion is committed by anyone who:

-

- provides false or incomplete information to the tax authorities,

- conceals facts relevant for taxation,

- or fails to use tax stamps as required,

and thereby evades taxes or obtains unjustified tax advantages.

Taxes are considered evaded “if they are not assessed, not assessed in full, or not assessed in a timely manner.” Section 370 (4) AO

Elements of the Offense: Objective & Subjective

Objective: Tax evasion occurs when one of the three forms of conduct under Section 370 AO is fulfilled:

-

- false or incomplete information provided to the tax office

- concealment of facts relevant for taxation

- failure to use prescribed tax stamps

… and thereby taxes are evaded or unjustified tax advantages are obtained (Section 370 (1) AO).

Subjective: Intent is required. Even conditional intent suffices, meaning: Anyone who considers the outcome possible and accepts it.

Intent – What Does This Mean Specifically?

Intent means not only knowledge but also acceptance of the consequences. In cases of:

-

- “Ignorance despite indications”

- “Failure to inquire despite gaps in knowledge”

conditional intent may already be present. Protective advice from a tax advisor only exonerates if the advisor was comprehensively informed.

BFH, VIII R 27/10: As a rule, the taxpayer may rely on the tax advisor preparing the tax return correctly and completely if the taxpayer has provided all information necessary for preparing the tax return. The taxpayer is generally not obligated to verify the tax return prepared by the tax advisor in every detail.

Penalty for Tax Evasion – Table & Overview

| Amount of Evasion | Possible Sanction |

|---|---|

| Under €1,000 | Dismissal possible |

| Up to €50,000 | Monetary penalty |

| From €50,000 | Particularly severe case, possibly imprisonment |

| From €100,000 | Imprisonment, usually suspended |

| From €1 million | Imprisonment without suspension |

Additionally:

-

- Entry in criminal record from 91 daily rates onwards

- Evasion interest: 0.5% per month

- Statute of limitations: 5 years, in particularly severe cases 10 years

Tax Evasion Penalties – Examples from Practice

| Case | Description |

|---|---|

| 1 | Self-employed person conceals income from cash sales |

| 2 | GmbH managing director falsifies travel expense receipts |

| 3 | Physician deducts private expenses as business costs |

| 4 | Online retailer fails to report sales correctly |

| 5 | Crypto investor conceals profits from trading |

| 6 | CFO manipulates balance sheets for bonus optimization |

| 7 | Influencer fails to declare social media advertising income |

| 8 | Undeclared wages in construction – no social security contributions, no tax |

| 9 | Restaurant owner without cash register fails to report sales |

| 10 | Dentist deducts privately rendered services as business expenses |

Voluntary Disclosure: The Last Exit

A complete, timely, and correct voluntary disclosure can lead to exemption from punishment (Section 371 AO).

Important:

-

- For an effective voluntary disclosure, all non-statute-barred tax offenses within the affected tax category must be fully declared retroactively – at a minimum for the last ten calendar years of that tax category.

- Payment of arrears + interest mandatory.

- We verify whether blocking grounds exist:

-

- Notification of audit

- Offense known

- Search already conducted

-

Have Your Voluntary Disclosure Prepared Legally Secure

At your side throughout Germany – with profound specialization in tax criminal law and economic criminal law.

Why Choose Us?

We are a nationwide law firm specializing in tax criminal law and economic criminal law.

Our clients benefit from:

-

- Over 1,000 defended proceedings in tax criminal law

- Specialist attorneys for criminal law & tax law

- Certified specialist advisors for tax criminal law

- Certified specialist advisors for economic criminal law

- Close collaboration with tax advisors

- Ongoing training in tax criminal law & current case law

Contact Us Now – Discreet & Experienced

Benefit from our expertise in tax criminal law for your defense – nationwide, discreet, and on equal footing.

Frequently Asked Questions About Influencers and Taxes

If you recognize possible unlawfulness but act nonetheless, this may suffice.

Yes, with proper structuring, exemption from punishment is then possible. We provide comprehensive support.

Depending on scope, circumstances, cooperation – often several months. In special cases, several years.

As a rule, imprisonment is threatened, which may be suspended under certain circumstances. The exact penalty depends on the amount, the conduct of the accused, and any mitigating factors.

Voluntary disclosure is excluded if a search has already taken place or the person concerned has been notified of the initiation of criminal proceedings.